Florida Title Company: Tips for Title Insurance

Title insurance is essential. It protects both buyers and lenders from issues that could render the title defective, or unforeseen hazards that challenge your right to the title. That’s why it’s important to hire a well-established title company to perform a title search, and to provide you with title insurance.

But how does insurance protect both parties? Whether you’re buying your first home, refinancing your current property, or are a realtor negotiating a sale, you need to understand the two types of title insurance.

Lender’s and Owner’s

The first type of title insurance is lender’s insurance, which is also known as mortgagee insurance, the lender’s policy, or the loan policy. As the name suggests, it protects your lender – typically your bank or mortgage broker.

Because the lender is helping to finance your real estate purchase, they have a vested interest in the transaction. Consequently, most lenders require the buyer to take out a loan policy as a prerequisite to the mortgage loan.

Mortgagee insurance, then, protects the lender’s investment in your property. In other words, the loan policy only covers the lender for the amount that is at risk for them, should problems arise with the title.

For example, if an undisclosed heir comes forward to lay claim to the property, the loan policy reimburses the lender the amount that was lent to the buyer. However, lender’s insurance can also be used to pay legal costs if the claim is disputable, which could save you from losing the property.

Keep in mind that the lender’s policy only lasts as long as you are repaying your mortgage loan. That’s why it’s also necessary to purchase owner’s insurance.

Owner’s insurance covers the buyer’s investment, and is purely for their benefit.

It protects them from the same contingencies as the lender’s loan – outstanding taxes, liens, fraudulent documents, and so on – but lasts as long as the owner has an interest in or obligation to the property. If the owner decides to sell that property, the new buyer will have to purchase their own title insurance.

The owner’s policy is a one-time payment, at the time of closing, in the same amount as the real estate purchase. Like lender’s insurance, it can also cover legal fees in the event of a lawsuit over the title.

Tips for Purchasing Title Insurance

- Remember that title insurance only covers issues relating to the title. It protects your right to the title and the investments involved in purchasing the property, but not the property itself. The buyer still needs to purchase home insurance to cover other damages.

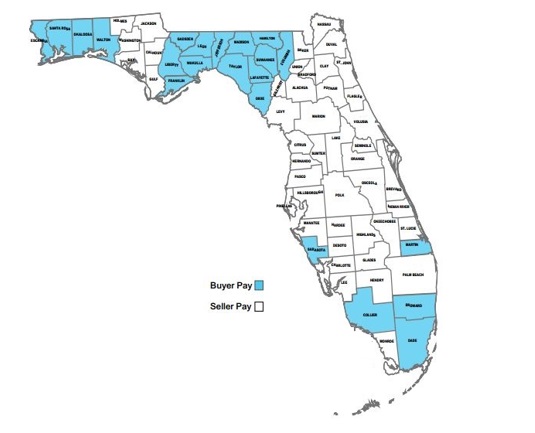

- Who pays which policy costs varies state-by-state. In Florida, who pays for the policy varies from County to County (see chart below). Sometimes the buyer pays all costs, and sometimes the seller covers some of the costs. Consult a professional title company for details on your state’s title insurance practices.

- Title insurance only covers the buyers and lenders for title issues that existed prior to the real estate transaction, whether they were disclosed or unforeseen. If, for example, you buy the property but fail to pay a contractor who does renovations for you, they may take out a lien against your home that is not covered by your title insurance.

- Always have a thorough title search performed before you purchase any property.

- Realtors can simplify the entire process by hiring the same company to perform the title search and write the title insurance policy. At Florida Home Title Company, we have the legal expertise to do both.

- Florida Home Title Company offers a discount if both policies are purchased at the same time. Contact us for further details.